Code

curve(dchisq(x, df = 10), from = 0, to = 40, xlab="X", ylab="f(X)", main = "Chi-squared density", sub = "(df = 10)")

The random variate \(X\) defined for the range \(0 \leq X \leq +\infty\), is said to have a Chi-squared Distribution with 1 parameter (i.e. \(X \sim \chi^2 \left( n \right)\)) with shape parameter \(n \in \mathbb{N}^+\).

\[ \text{f}(X) = \frac{ X^{\frac{n}{2}-1} e^{- \frac{X}{2} } }{ 2^{\frac{n}{2}} \mathrm{ \Gamma} \left[ \frac{n}{2} \right] } \]

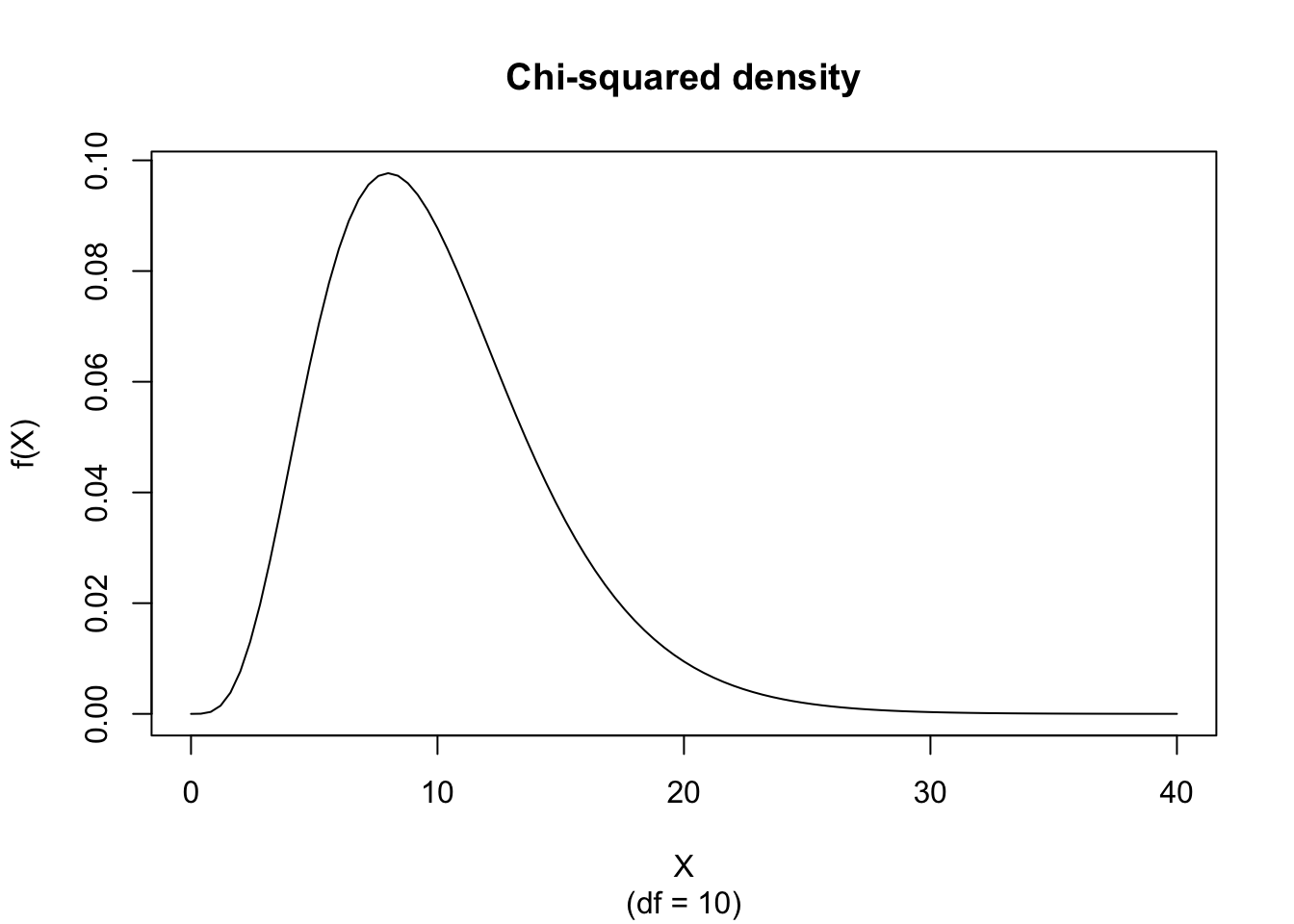

The figure below shows an example of the Chi-squared Probability Density function with \(df = 10\).

curve(dchisq(x, df = 10), from = 0, to = 40, xlab="X", ylab="f(X)", main = "Chi-squared density", sub = "(df = 10)")If \(n/2 \notin \mathbb{N}^+\) then there is no closed form. If \(n/2 \in \mathbb{N}^+\) then

\[ \text{F}(X) = 1 - e^{-\frac{X}{2}} \sum_{j=0}^{r-1} \frac{\left( \frac{X}{2} \right)^j}{j!} \]

where \(r = \frac{n}{2}\).

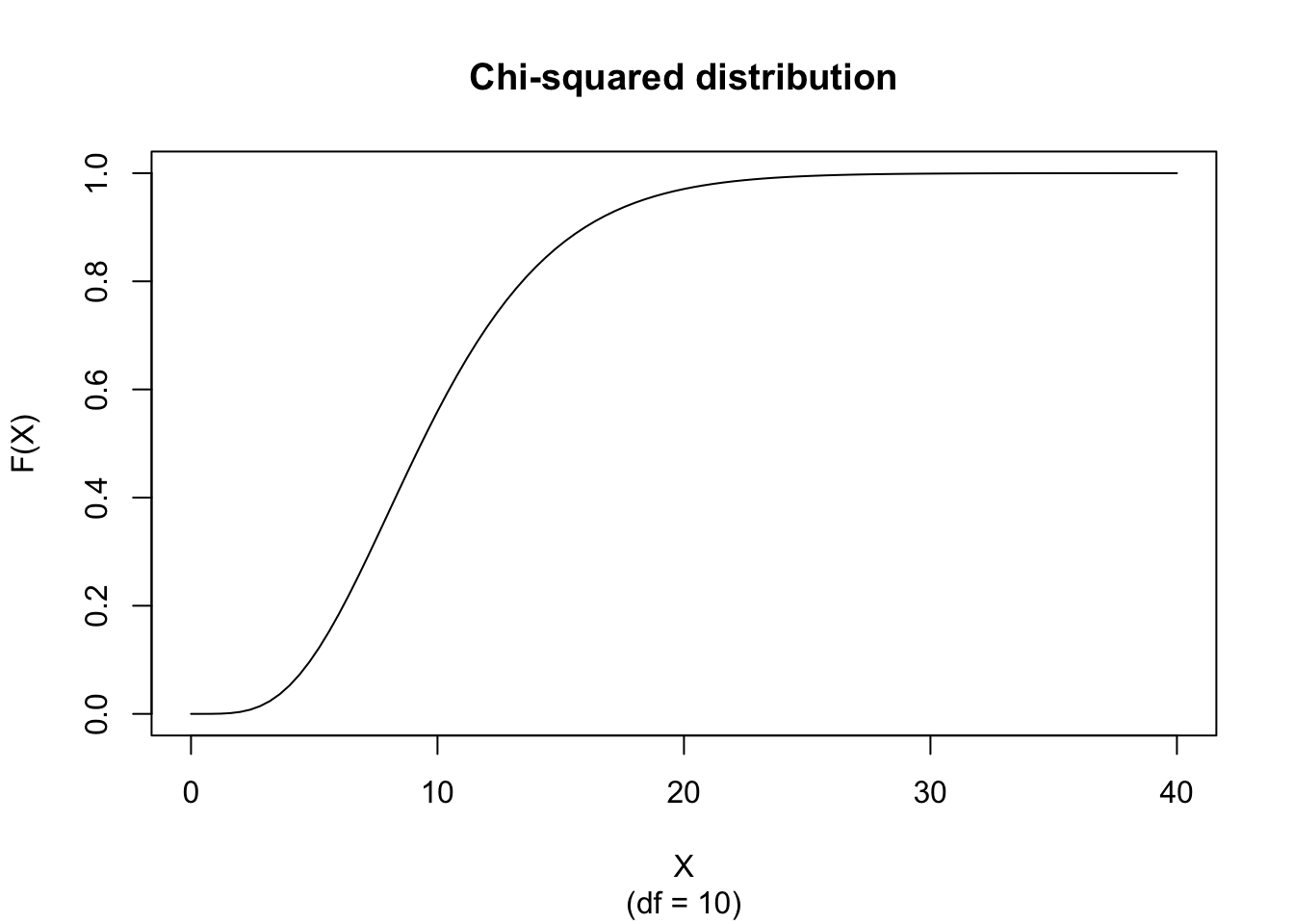

The figure below shows an example of the Chi-squared Distribution with \(df = 10\).

curve(pchisq(x, df = 10), from = 0, to = 40, xlab="X", ylab="F(X)", main = "Chi-squared distribution", sub = "(df = 10)")

\[ \text{M}_X(t) = (1-2t)^{-\frac{n}{2}} \]

for \(t < \frac{1}{2}\).

\[ \mu_j' = 2^j \frac{\mathrm{\Gamma}\left[ \frac{n}{2}+j \right]}{\mathrm{\Gamma}\left[ \frac{n}{2} \right]} \]

\[ \text{E}(X) = n \]

\[ \text{V}(X) = 2n \]

\[ \text{Mo}(X) = n - 2 \]

for \(n \geq 2\).

\[ g_1 = 2 \sqrt{\frac{2}{n}} \]

\[ g_2 = 3 + \frac{12}{n} \]

\[ VC = \sqrt{\frac{2}{n}} \]

The best fitting Chi-squared Density function can be obtained by estimating the degrees of freedom \(n\) according to the so-called Maximum Likelihood procedure which can be found on the public website:

The Maximum Likelihood Fitting for the Chi-squared Distribution is also available in RFC under the menu “Distributions / ML Fitting” (you have to select the appropriate function in the designated “Density Function” drop menu).

If you prefer to compute the Chi-squared ML fitting on your local computer, the following code snippets can be used in the R console:

library(MASS)

library(car)

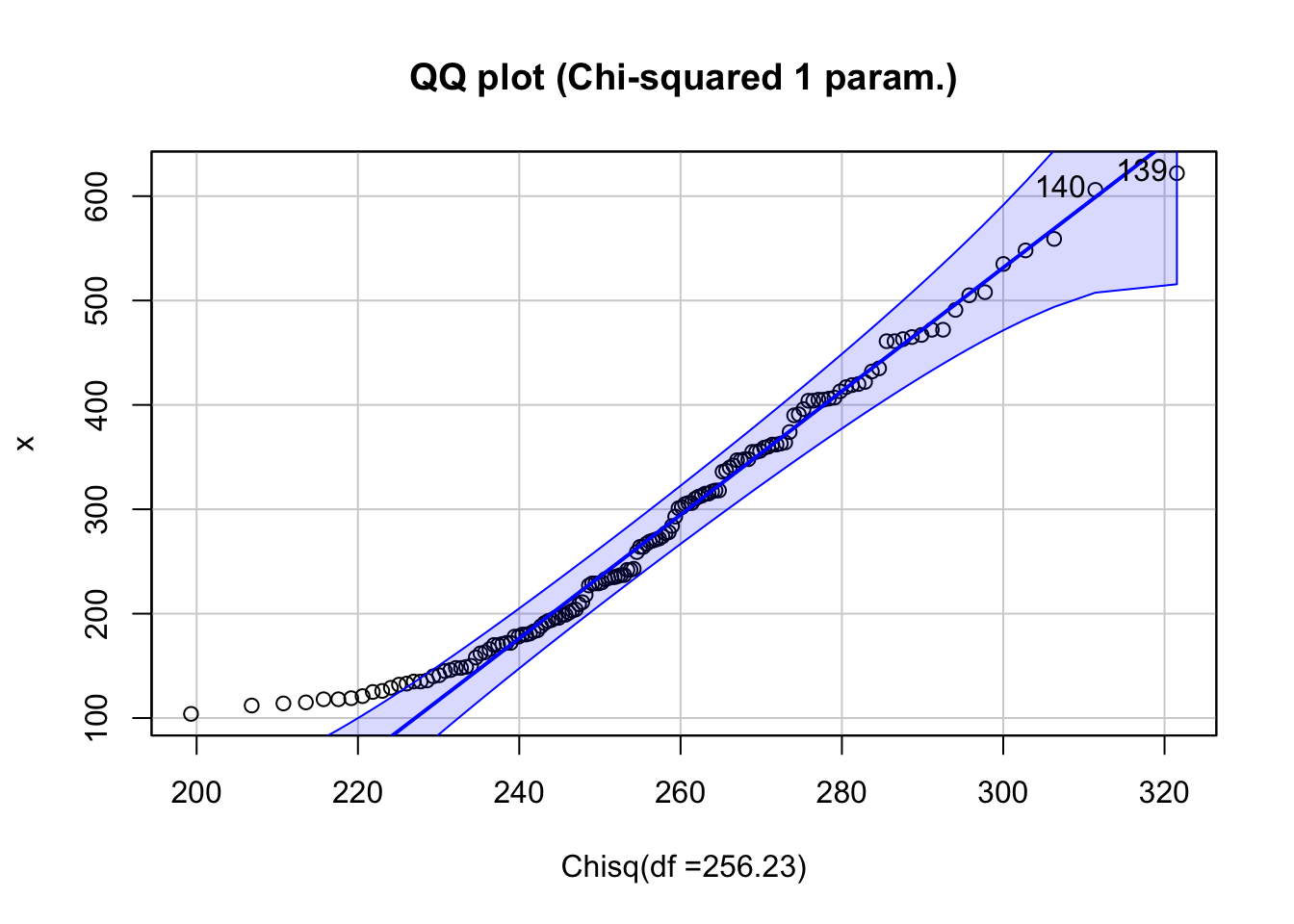

x <- as.numeric(AirPassengers)

chi_df <- fitdistr(x, 'chi-squared', start = list(df=3), method = 'Brent', lower = 0.1, upper = 10000)

chi_k <- chi_df[[1]][1]

cat("estimated df = ", chi_df$estimate, "\n")

cat("standard deviation = ", chi_df$sd, "\n")estimated df = 256.2321

standard deviation = 1.882792 and

xlab <- paste('Chisq(df =', round(chi_df$estimate[[1]],2),')', sep = '')

qqPlot(x, dist = 'chisq', df = chi_df$estimate[[1]], ncp = 0, main = 'QQ plot (Chi-squared 1 param.)', xlab = xlab )[1] 139 140

The main function in this R script is fitdistr and is limited by the user-specified lower and upper limit. Instead of displaying a histogram, the script calls the qqPlot function from the car library. The interpretation of this plot is explained in Descriptive Statistics.

We analyze the time series of monthly divorces (in thousands) and wish to find out whether it can be adequately described by the Chi-squared Distribution. The ML Fitting module can be used to find the best fitting Chi-squared Distribution for the divorces data.

The estimated degrees of freedom is \(n = 3.46\) but the Chi-squared distribution does not fit the data well (as is shown in the Figure). The visual evidence suggests that a Chi-squared density is not appropriate for these data; for formal goodness-of-fit testing, see Section 2, Section 124.1, and Chapter 125.

If the following is true

\[ \begin{align*} \begin{cases} \text{U}(0,1) \text{ denotes a Uniform Distribution} \\ \text{N}(0,1) \text{ denotes a Standard Normal Distribution} \end{cases} \end{align*} \]

then \(\chi^2(n) \sim -2 \text{ln} \left( \prod_{i=1}^{r} \text{U}_i(0,1) \right)\) with \(r=\frac{n}{2}\) and \(n\) is even

and \(\chi^2(n) \sim -2 \ln \left( \prod_{i=1}^{r} \text{U}_i(0,1) \right) + \left( \text{N}\left( 0, 1 \right) \right)^2\) with \(r=\frac{n-1}{2}\) and \(n\) is odd