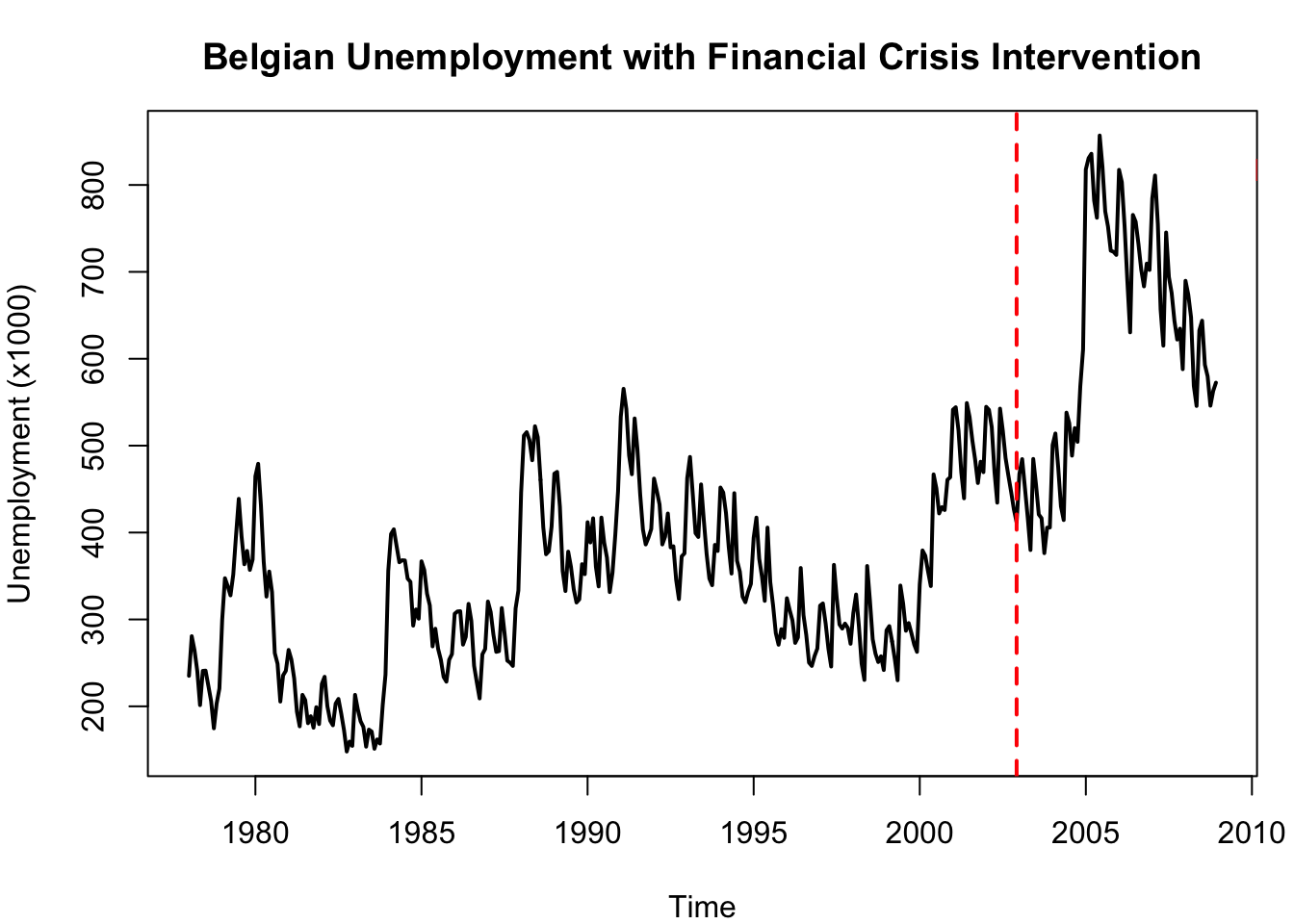

# Unemployment data (from BJ.qmd)

unemployment <- c(235.1, 280.7, 264.6, 240.7, 201.4, 240.8, 241.1, 223.8,

206.1, 174.7, 203.3, 220.5, 299.5, 347.4, 338.3, 327.7, 351.6, 396.6,

438.8, 395.6, 363.5, 378.8, 357, 369, 464.8, 479.1, 431.3, 366.5,

326.3, 355.1, 331.6, 261.3, 249, 205.5, 235.6, 240.9, 264.9, 253.8,

232.3, 193.8, 177, 213.2, 207.2, 180.6, 188.6, 175.4, 199, 179.6,

225.8, 234, 200.2, 183.6, 178.2, 203.2, 208.5, 191.8, 172.8, 148,

159.4, 154.5, 213.2, 196.4, 182.8, 176.4, 153.6, 173.2, 171, 151.2,

161.9, 157.2, 201.7, 236.4, 356.1, 398.3, 403.7, 384.6, 365.8, 368.1,

367.9, 347, 343.3, 292.9, 311.5, 300.9, 366.9, 356.9, 329.7, 316.2,

269, 289.3, 266.2, 253.6, 233.8, 228.4, 253.6, 260.1, 306.6, 309.2,

309.5, 271, 279.9, 317.9, 298.4, 246.7, 227.3, 209.1, 259.9, 266,

320.6, 308.5, 282.2, 262.7, 263.5, 313.1, 284.3, 252.6, 250.3, 246.5,

312.7, 333.2, 446.4, 511.6, 515.5, 506.4, 483.2, 522.3, 509.8, 460.7,

405.8, 375, 378.5, 406.8, 467.8, 469.8, 429.8, 355.8, 332.7, 378,

360.5, 334.7, 319.5, 323.1, 363.6, 352.1, 411.9, 388.6, 416.4, 360.7,

338, 417.2, 388.4, 371.1, 331.5, 353.7, 396.7, 447, 533.5, 565.4,

542.3, 488.7, 467.1, 531.3, 496.1, 444, 403.4, 386.3, 394.1, 404.1,

462.1, 448.1, 432.3, 386.3, 395.2, 421.9, 382.9, 384.2, 345.5, 323.4,

372.6, 376, 462.7, 487, 444.2, 399.3, 394.9, 455.4, 414, 375.5,

347, 339.4, 385.8, 378.8, 451.8, 446.1, 422.5, 383.1, 352.8, 445.3,

367.5, 355.1, 326.2, 319.8, 331.8, 340.9, 394.1, 417.2, 369.9, 349.2,

321.4, 405.7, 342.9, 316.5, 284.2, 270.9, 288.8, 278.8, 324.4, 310.9,

299, 273, 279.3, 359.2, 305, 282.1, 250.3, 246.5, 257.9, 266.5,

315.9, 318.4, 295.4, 266.4, 245.8, 362.8, 324.9, 294.2, 289.5, 295.2,

290.3, 272, 307.4, 328.7, 292.9, 249.1, 230.4, 361.5, 321.7, 277.2,

260.7, 251, 257.6, 241.8, 287.5, 292.3, 274.7, 254.2, 230, 339,

318.2, 287, 295.8, 284, 271, 262.7, 340.6, 379.4, 373.3, 355.2,

338.4, 466.9, 451, 422, 429.2, 425.9, 460.7, 463.6, 541.4, 544.2,

517.5, 469.4, 439.4, 549, 533, 506.1, 484, 457, 481.5, 469.5,

544.7, 541.2, 521.5, 469.7, 434.4, 542.6, 517.3, 485.7, 465.8, 447,

426.6, 411.6, 467.5, 484.5, 451.2, 417.4, 379.9, 484.7, 455, 420.8,

416.5, 376.3, 405.6, 405.8, 500.8, 514, 475.5, 430.1, 414.4, 538,

526, 488.5, 520.2, 504.4, 568.5, 610.6, 818, 830.9, 835.9, 782,

762.3, 856.9, 820.9, 769.6, 752.2, 724.4, 723.1, 719.5, 817.4, 803.3,

752.5, 689, 630.4, 765.5, 757.7, 732.2, 702.6, 683.3, 709.5, 702.2,

784.8, 810.9, 755.6, 656.8, 615.1, 745.3, 694.1, 675.7, 643.7, 622.1,

634.6, 588, 689.7, 673.9, 647.9, 568.8, 545.7, 632.6, 643.8, 593.1,

579.7, 546, 562.9, 572.5)

unemp_ts <- ts(unemployment, start = c(1978, 1), frequency = 12)

# Step intervention at the financial crisis (around observation 300, late 2008)

T_crisis <- 300

step_crisis <- c(rep(0, T_crisis - 1), rep(1, length(unemployment) - T_crisis + 1))

# Fit ARIMA with intervention (using same order as in estARIMA.qmd)

fit_unemp <- arima(sqrt(unemp_ts),

order = c(2, 1, 1),

seasonal = list(order = c(0, 1, 1), period = 12),

xreg = step_crisis)

cat("ARIMA(2,1,1)(0,1,1)[12] with financial crisis intervention:\n")

print(fit_unemp)