Code

x <- seq(-7,7,length=1000)

hx <- dt(x, df = 5)

plot(x, hx, type="l", xlab="X", ylab="f(X)", xlim=c(-7,7), main="Student t density", sub = "(n = 5)")

The random variate \(X\) defined for the range \(-\infty \leq X \leq +\infty\), is said to have a Student t-Distribution (i.e. \(X \sim \text{t} \left( n \right)\)) with shape parameter \(n \in \mathbb{N}^+\).

\[ f(X) = \frac{\Gamma \left[ \frac{n+1}{2} \right]}{\Gamma \left[\frac{1}{2}\right] \Gamma \left[ \frac{n}{2} \right] } n ^{-\frac{1}{2}} \left[ 1 + \frac{X^2}{n} \right]^{-\frac{n+1}{2}} \]

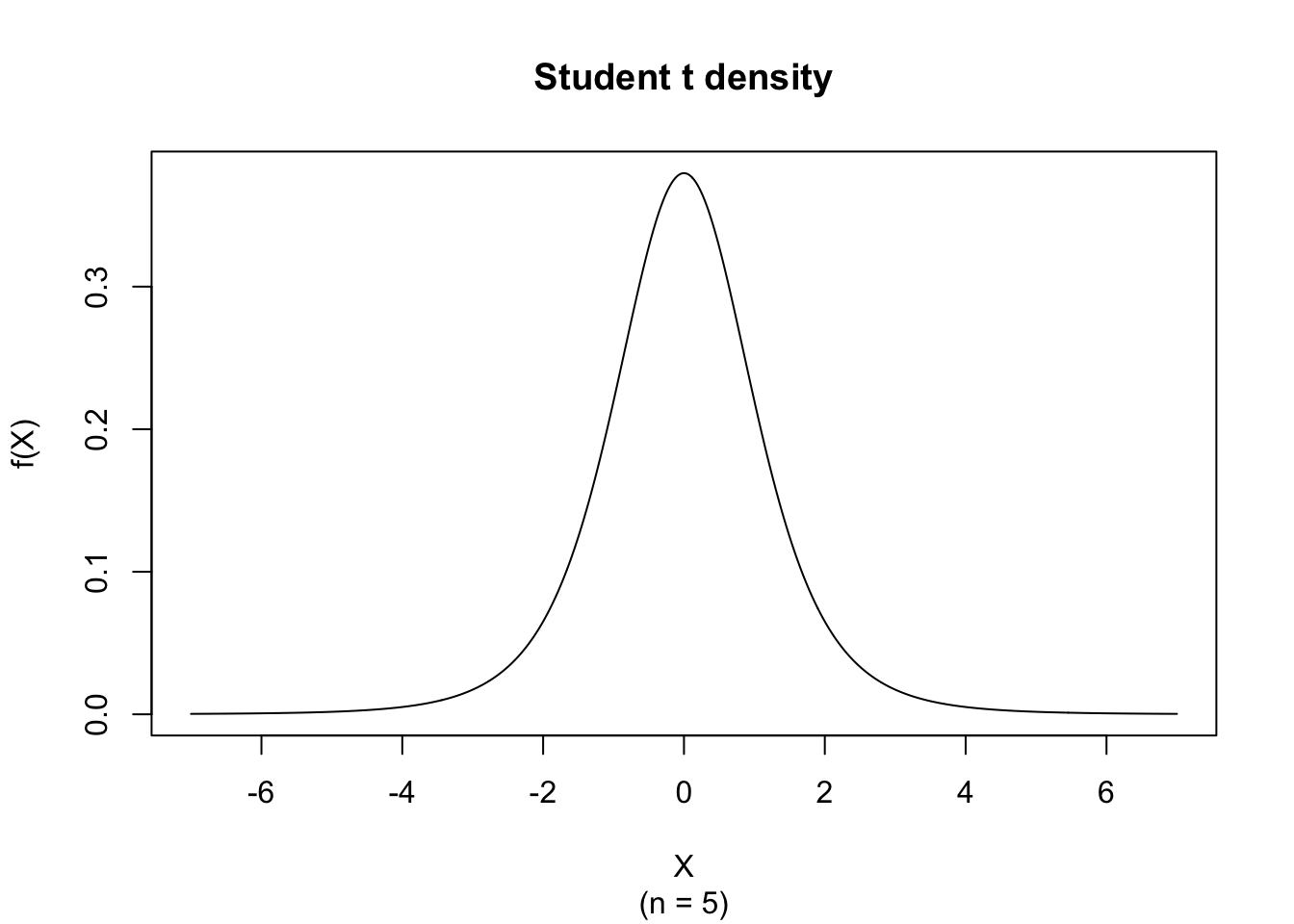

The figure below shows an example of the Student t Probability Density function with \(n = 5\).

x <- seq(-7,7,length=1000)

hx <- dt(x, df = 5)

plot(x, hx, type="l", xlab="X", ylab="f(X)", xlim=c(-7,7), main="Student t density", sub = "(n = 5)")\[ \begin{align*} \mu_j &= 0 & \text{ j odd}\\ \mu_j &= n^{\frac{j}{2}} \frac{\text{B}\left[ \frac{j+1}{2}, \frac{n-j}{2} \right]}{\text{B}\left[ \frac{1}{2}, \frac{n}{2} \right]} & \text{ j even and } j < n \\ \mu_4 &= n^2 \frac{3}{(n-2)(n-4)} & n > 4 \end{align*} \]

\[ \text{E}(X) = 0 \]

for \(n > 1\).

\[ \text{V}(X) = \frac{n}{n-2} \]

for \(n > 2\) (undefined otherwise).

\[ \text{Med}(X) = 0 \]

\[ \text{Mo}(X) = 0 \]

\[ g_1 = 0 \]

for \(n > 3\) (undefined otherwise).

\[ g_2 = \frac{3n - 6}{n-4} \]

for \(n > 4\). Note that since \(\lim\limits_{n \rightarrow +\infty} g_2(n) = 3\), it follows that the Kurtosis of the t-Distribution is larger than the Kurtosis of the Normal Distribution.

There is a relationship between the t-Distribution with parameter \(n\) (degrees of freedom), denoted by t\((n)\), the unit normal variate N(0,1), and the Chi-squared Distribution with parameter \(n\), denoted by \(\chi^2(n)\):

\[ X = \frac{\text{N}(0,1)}{\sqrt{\frac{\chi^2(n)}{n}}} \sim \text{t}(n) \]

For \(n \geq 30\) the t-Distribution, denoted by t\((n)\), approximates the Standard Normal Distribution.

Suppose we need the critical value for a two-sided 95% confidence interval with 12 degrees of freedom. We compute:

qt(0.975, df = 12)[1] 2.178813If we also want the tail probability for an observed test statistic \(t = 2.1\) (with 12 degrees of freedom), we can compute:

2 * (1 - pt(abs(2.1), df = 12))[1] 0.05754494The Student t-Distribution is used for inference on means when the population variance is unknown and must be estimated from the sample. It is central to one-sample, paired-sample, and independent two-sample t-tests, and to confidence intervals for means in small to moderate samples.